Since several were not fond of Game theory as a tool of explaining price action, I will instead directly explain why a saturationFlag is critical to minimizing rebase error, using Supply and Demand Curves as well as using Control Theory, which is literally used in the real world to solve problems identical to this.

UNDERSTANDING SUPPLY AND DEMAND W.R.T. REBASE

First we establish that for Ampl, there exists a demand curve which slopes down, like any other asset. And because the cost of producing AMPL’s is low, the supply curve is essentially vertical. This is explained in the Redbook.

When price is neutral we are at Price target PT, and supply does not change when we are within threshold.

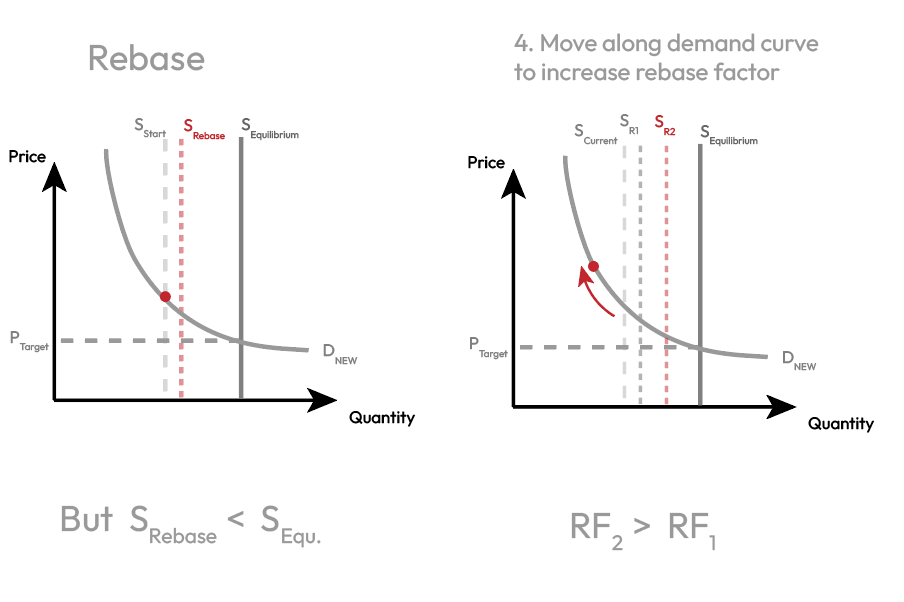

In the absence of any real demand via a new utility, etc. Any price action is directed towards moving along the demand curve. I.e. If we go above threshold, we move up along the demand curve. When the protocol observes it’s price information, it increases the supply. This is the rebase.

The market takes time to realize the discrepancy between the current supply and the true supply needed for equilibrium which leads to the price swinging below target to nudge the supply back into place. The rebase serves as an error correction mechanism to bring the price back to it’s target.

UNDERSTANDING DEMAND CURVE SHIFTS

In economic supply & demand theory, we shift the curve when demand changes for any reason other than price. (I.e. launch of a new utility). This means that our equilibrium supply for target price is somewhere much higher than the old equilibrium. This causes a sudden increase in the price when the market realizes the need for a larger supply for equilibrium. (This is the RIP).

Now even though the price is above target, we only rebase proportional to 1/10th of the price delta. So when the market realizes that the supply is still not growing fast enough, the market moves along the demand curve, further increasing the price.

As a result the rebase factor grows, and we get closer to the equilibrium supply faster. The market has determined that its more efficient to pay a higher price in order to get the supply to where it needs to be sooner. You may ask why the price doesn’t go to infinity, and that’s because there’s a price at which the need for getting to destination supply as soon as possible no longer outweighs the short term interest to sell. During Defi Summer this price was ~$4.

Unfortunately, the market takes time to react, so once we do arrive at the equilibrium supply- the price is still elevated, well beyond it’s target level. And by the time the market has realized that supply has been reached, we will still be rebasing positively, well beyond the target supply. This is the error. This is the cause for the FLIP.

Some have brought up why we do not rebase continuously, and now you can imagine, the error would be MUCH larger than if it was once a day. This is because you would be applying the entire rebase from the old equilibrium to the new equilibrium at once, and by the time the market realizes, the error will have grown way too far.

If the market wants to get the supply back to it’s equilibrium levels, the price needs to swing well below target, long enough to nudge the supply back to it’s right spot. Hence the long periods of negative rebase (i.e. the DIP & TRIP)

Therefore if we want to maximize the time Ampl is at it’s target price, we must minimize the error.

SIGMOID FUNCTION

Sigmoid function helps with this. If there is a sudden shift of the demand curve, the market will not pay more than the Saturation price. This is the price at which rebase curve begins to flatten. This is because moving the price higher does not make the rebases go any faster. It will however take longer to get to the target supply. This is fine, because our goal is to minimize the error.

Once we arrive to the target supply, the error will now be much less than if we had a linear function, since the price will not have run away drastically. It shouldn’t be significantly higher than the saturation price.

However there will still be significant error. Note that despite the rebase factor being relatively constant above saturation price, the amount of supply adjustment each day is still accelerating. This is because even though the Rebase factor is constant, the supply adjustment is calculated as RF * Current supply (which is a growing number with each day).

Once again, since the market takes time to react- the error will be growing by the time the equilibrium supply is reached. Also, there’s no evidence that the market will slow down approaching target. If that were the case then we would not have seen a contraction post-Defi-Summer. This is the case in ALL markets. This is why there’s blow-off tops in other crypto assets too. It’s not a coincidence.

This is like trying to stop a truck that’s accelerating up to 100mph into a parking spot accurately. Ultimately there will be error and we will need to contract a significant amount back to the intended supply.

How can we fix this?

The following strategy is often implemented in the real world with PID controllers.

This article explains how AMPL and other protocols use Feedback control.

In this example, you have the following:

|

|

|

1. There’s a drone that you hold, which has a sensor that measure the error between its current height and destination height. |

|

2. You turn on the propellers, but you don’t release the drone until the propellers are spinning at the saturation speed. |

|

3. When you finally release the drone, it flies way higher than it’s intended target because while you were holding it down, integral error signal was accumulating, and keeps accumulating even after passing the target. It then takes a long time to correct and come back down to it’s intended target. |

|

4. The solution is to modify the controller to detect if the signal before and after saturation limit is the same. This lets the controller know if it’s at saturation levels |

|

5. The controller checks if the sign of the error signal and the command signal are opposite signs.

|

|

6. If both 4. and 5. are true then the controller’s integrator is turned off. |

If we truly want to minimize error, the protocol needs to know that it was operating at saturated prices and that the subsequent price drop is likely reflective of the market taking time to come back to the target price.

This can be implemented by the following:

- If we set a flag at saturation price, then the protocol can be aware that it is within saturation conditions

- If the price drops after reaching saturation levels, then it can shut off the rebase

- We can discuss whether the flag is better to be reset when Ampl:

- Gets back to target price

- Comes below saturation price

The argument that this would make the protocol break is akin to saying that integral-wind up correction breaks drones. It’s simply not based on logic or relevant evidence. If anyone sees a problem with this, I would appreciate an example of a specific scenario where this would break.

If we truly wanted to minimize error even further, we can ask ourselves whether it even makes sense for supply adjustments to accelerate when in saturation? Perhaps we have a constant supply adjustment once saturation levels are met? i.e. it’s easier to stop a car that’s moving at a constant speed than one that’s accelerating. In the real world, objects have terminal velocity due to air resistance.

It’s worth noting that these flags are irrelevant to Ampl in the absence of the demand curve shifting. They only come into play when there is a sudden shock in demand. We’ve seen how Ampl performs in those scenarios (i.e. Defi Summer). You might say that AMPL’s not broken because it reached its target price after Defi summer. But if you drive your car too fast into a red light and don’t back-track until you’re already deep into the intersection, that’s far more dangerous.

In all of these examples, it was looking at demand shocks to the upside, but same logic applies to the downside.